If you apply before the 30th of June …

Applications for the SME Business Recovery Loan Scheme close on 30th June 2022

So if you could use 5-year fixed-rate finance, plan to have your application in by June 2022

The SME Business Recovery Loan Scheme offers low interest loans capped at 7.5% to SME businesses with a turnover of $750,000 or more AND it’s government guaranteed, so it doesn’t require real estate as security

That’s a pretty good deal…

The application process is even simpler than a credit card application

All you need is:

Company Name and ABN

Company Address

Bank statements (read only link to company trading account)

Directors details

Name and address and a photo of driver licence

How easy is that !?!

How much can you borrow?

If you meet the turnover requirements, then you can:

Borrow from $50,000 – $500,000

Borrow up to 1.5x your monthly average turnover (the limit)

How does it work?

What you get is a revolving Line of Credit with a redraw facility that can be used to pay domestic and overseas suppliers.

The mechanics of the process include:

- A straightforward online application process.

- Fast Approval.

- An online customer portal where you upload customer invoice & supplier payments.

Key Qualifying Criteria

You quality if:

- You’ve been trading for a minimum of one (1) year

- Your minimum business turnover is $700k pa

- Clear Credit & Repayment History

- The facility is to pay supplier invoices and subcontractors

NOTE: If your turnover is over $500,000 then it might be worth exploring with an expert – because if you can show that your business is growing and will reach $700.000 in the next 6 months then you could possibly qualify.

What are the costs and charges?

(Maximum loan amount is limited to $500,000)

So what you’re up for is:

- Establishment Fee: $795 (one-off set up fee)

- Monthly Fee: $75 per month

- Interest Rate: 7.50% pa

- Payment Fee: 1.95% (on payment, ONLY on funds drawn)

Compared with a typical FinTech loan, with credit-card level interest rates that can range from 15% to 25% this is a pretty good deal.

I have clients using this facility to:

- Refurbish their restaurant

- To grow an NDIS provider by paying his subcontractors

- Stock up on optical fibre cable to avoid supply chain disruption

- Buy in extra solar panels to avoid price rises

What’s the Line of Credit Repayment Process?

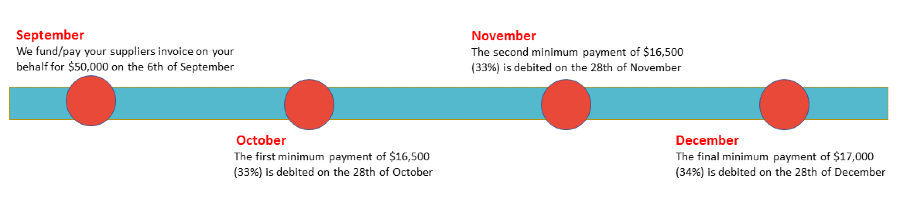

The repayment terms (minimum payments) for the Moneytech Facility is 33%, 33%, and 34%. After we fund the invoice payment using the facility, the first minimum payment of 33% will be due on the 28th of the following month. The next 33% will be due on the 28th of the next month, and the final 34% on the 28th following.

Normally due payments will be direct-debited from a nominated bank account on the due date (28th of each month), However, EFT, BPAY and Credit Card payments prior to the due date are also available.

What are the terms and conditions?

Terms

There is No Minimum Term and No Lock-in Contract

Security

1. Any Ranking General Security Agreement (GSA).

2. Director & Shareholder Personal Guarantees.

What can you fund with the money?

This can be used to purchase International & Domestic suppliers for:

- Stock

- Materials

- Equipment

You can also use the funds for:

- Subcontractors

- Bills

- Stock

Basically, if you need to spend money to kickstart your business post-COVID then this can fund it.

What information do you need to get your application underway

By finance industry standards, this is no more difficult than applying for a credit card. You need some basic Company information and director details. You also need to supply Trust details if you have an associated Trust.

Basic Company information

The basic information about your business that’s needed.

- Amount of Finance required $

- ABN

- Full Company Name

- Trading name if applicable

- Trading address

- Telephone number

- Website

Directors details

Basic directors details for each director of the company

- Full Name

- Residence address

- Email address

- Phone number

- Home buying status (ie. are you buying a home?)

- Do you have any other properties?

- Drivers license scan or picture front and back

Trust details

If there is a trust in place then you need to supply:

- Details of the beneficiaries

- Copy of the trust deed

Escape the post-COVID cash trap

Don’t let your business be hamstrung by working capital limitations post-COVID.

If you qualify for the SME Business Recovery Loan Scheme then act fast (like today).

Your first step is as easy as a phone call

Don’t let the “get around to it” gremlins (or the rush to get sales today) rob you of this opportunity.

Phone or message me today – or book a call here:

https://calendly.com/martincattach/sme-loan-recovery-scheme-discovery-meeting

That will put an appointment in both our diaries, as well as a spanner in the works of the “get around to it” gremlins.

Call us even if you DON’T qualify

If you don’t qualify, then talk to us anyway – because the post-COVID cash trap is getting closer.

January, February and March 2022 could well be a “valley of death” for many COVID-reduced businesses who aren’t prepared for the full impact of the cash gap (the delay between what they’re owed and when they’ll get paid)

Link to Cash Trap Article:

https://finforbiz.com.au/the-post-covid-cash-trap-and-how-to-avoid-it/

We’re working capital specialists and our experts specialise in finding ways for SME businesses to escape the cash trap – without mortgaging their future to exorbitant FinTech Interest rates.

Martin Cattach

+61 407 477 555

Discussion on working capital and funding options:

https://calendly.com/martincattach/confidential-discussion-on-working-capital-requirements